Easy import Data

Bulk Pan Verification

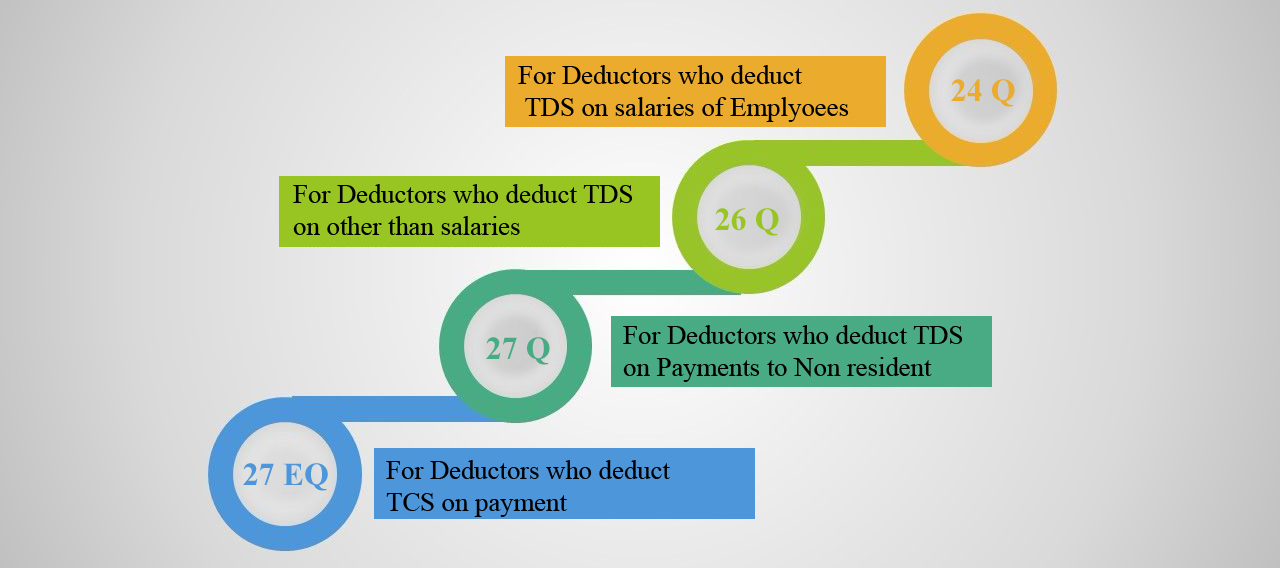

Return Preparation

Automatic Calculations of TDS

Return Uploading

Generation of Form 16

Legal Queries & Support Services.

Sections, Rates & Threshold Limits

| Section | Particulars | TDS Rates in % | Threshold Limits |

| 192 | Salary | As per the rates of Income Slab | As per the rates of Income Slab |

| 192A | Payment of accumulated balance of provident fund which is taxable in the hands of an employee | 10 | – |

| 193 | Interest on securities | ||

| a) Interest on Securities | 10 | Nil | |

| b) Interest on Debentures; | 10 | Nil | |

| 194 | Dividend (other than the listed companies) |

10 | Nil |

| 194A | Income by way of interest other than interest on securities | 10 | Rs. 5,000 |

| 194B | Winnings from lotteries/ puzzles/card games. | 30 | Rs. 10,000 |

| 194BB | Income by way of Winnings from horse races | 30 | Rs. 5,000 |

| 194C | Payment to contractor/sub- contractor a) HUF/Individuals b) Others |

1 2 |

Rs. 30,000 |

| 194D | Insurance commission | 5 | Rs. 20,000 |

| 194DA | Payment in respect of life insurance policy | 1 | – |

| 194EE | Payment of NSS Deposits | 10 | Rs. 2,500 |

| 194F | Payment on account of repurchase of unit by Mutual Fund or Unit trust of India | 20 | Nil |

| 194G | Commission on sale of lottery tickets | 5 | Rs. 1,000 |

| 194H | Commission or brokerage | 5 | Rs. 5,000 |

| 194-I | Rent a) Plant & Machinery b) Land or building or furniture or fitting |

2 10 |

Rs. 1.8 lakhs |

| 194-IA | Payment on transfer of certain immovable property other than agricultural land | 1 | – |

| 194-IB | Payment of rent by individual or HUF not liable to tax audit | 5 | – |

| 194-IC | Payment of monetary consideration under Joint Development Agreements | 10 | – |

| 194J | Any sum paid by way of a. Fee for professional services b. Fee for technical services c. Royalty d. Remuneration/fee/commission to a director or e. For not carrying out any activity in relation to any business f. For not sharing any know-how, patent, copyright etc. |

10 | Rs. 30,000 |

| 194LA | Payment of compensation on acquisition of certain immovable property | 10 | Rs. 1 lakh |

| 194LBA | Income distribution by a Business Trust u/s 115UA | 10 | – |

| 194LBB | Income distribution by a Investment Fund u/s 115UB | 10 | – |

| 194LBC | Income distribution by a Securitisation Trust u/s 115TCA | 25% in case of Individual or HUF 30% in case of other individual | – |

| Any other Income | 10 | – |